Collateral Damage Haircut

A repurchase, or repo, agreement involves a borrower selling a bunch of securities for cash and agreeing to buy them back later for a higher price. The difference between the two prices represents the interest payment. The market is huge: a survey by the International Capital Market Association estimated that, in June this year, European repo agreements were worth €5.6 trillion ($6.4 trillion).

WHEN the financial system teetered on the brink of collapse in 2008, the biggest problem was a lack of liquidity. Banks were unable to refinance themselves in the short-term debt markets. Central banks had to step in on a massive scale to offer support. Calm was eventually restored, but not without enormous economic damage.

But has the underlying problem of liquidity gone away? A research note from Michael Howell of Crossborder Capital argues that, in the modern financial system, central banks are no longer the only, or even the main, providers of liquidity. Instead, the system looks a lot like that of the Victorian era, with banks dependent on the wholesale markets for funding. Back then, the trade bill was the key asset for bank financing; now it is the mysteriously named “repo” market.

To borrow in the repo market, banks need assets to pledge against the loans—collateral, in other words. And, Mr Howell argues, it is the supply of, and demand for, collateral that determines liquidity in the financial markets.

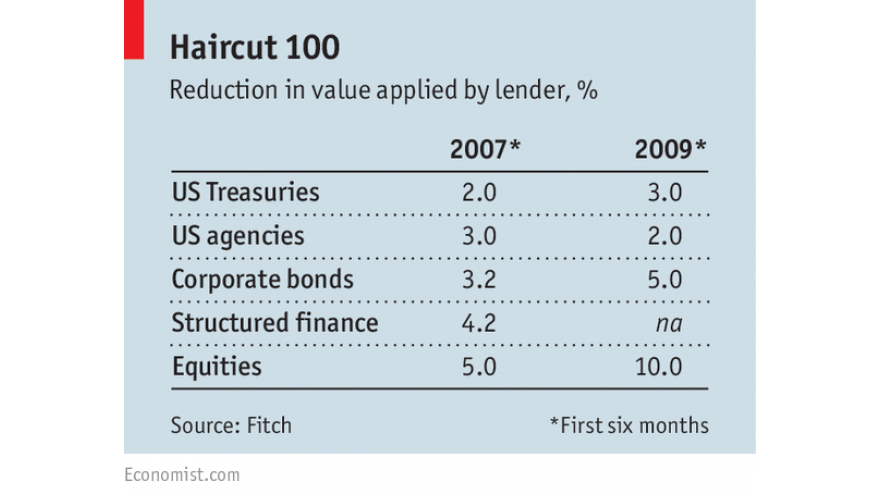

The problem is that not all collateral is treated equally. Lenders worry that, if the borrower fails to repay, the securities they are left holding may not sell for their face value. So they apply a discount, or “haircut”, to the collateral, depending on its perceived riskiness. At times of stress, lenders get nervous and apply bigger discounts than before. This is what happened during the financial crisis (see table).

Bigger haircuts mean that borrowers need more collateral than before in order to fund themselves. “When market volatility jumps, funding capacity drops in tandem and often substantially,” writes Mr Howell. The result, a liquidity squeeze at the worst possible moment, is a template of how the next crisis may occur (although regulators are trying to reduce banks’ reliance on short-term funding).

Viewed in this light, global liquidity should not be measured merely by the size of central banks’ balance-sheets but by the availability of acceptable collateral as well. On Mr Howell’s calculations, global collateral shot up in the aftermath of the financial crisis, but grew much more slowly from 2012 onwards. This may explain why global growth has been so sluggish.

Traditional quantitative easing may do little to help. “Simply expanding the central bank balance-sheet by buying in Treasuries from the private sector is robbing Peter to pay Paul,” writes Mr Howell, since the bonds could have anyway been used as collateral for repo transactions.

Given that funding conditions resemble those in Victorian times, Mr Howell thinks that central banks should return to the policies favoured by Walter Bagehot, a former editor of this newspaper, and focus, above all, on the smooth running of the credit markets. If they do not, the risk is that a shortage of collateral may induce another funding squeeze; low as they are, government-bond yields may then fall even further as banks scramble to get hold of them for funding purposes.

This view is an interesting contrast with a popular investment theme of the moment—the idea of “quantitative tightening” (QT). Central banks are slowing their pace of asset purchases; China has been offloading some foreign-exchange reserves. Since many people think that central-bank purchases have been propping up the financial markets, their fear is that QT may cause bond yields to rise in the absence of central-bank support.

These differing interpretations point to the difficulty of analysing a broad concept like “global liquidity”. It is reminiscent of the problem of defining the money supply during the heyday of monetarism in the late 1970s and early 1980s. Everyone can agree that notes and coins are money but the wider the definition, the greater the scope for disagreement. Use the wrong measure, and the monetary signals may completely mislead. A fast-changing financial system makes things even harder: how does Bitcoin fit into global liquidity calculations?

Such complexity makes the withdrawal of monetary stimulus by central banks even more difficult. The IMF warned in a paper last year that “central banks’ exit strategy needs to be mindful of disruptions to the financial plumbing”. Even if they manage that trick, Mr Howell is surely right. One day the financial headlines will be dominated by worries about a collateral shortage.

Comments