Quantitative frightening

Controlling for the range of things that influence interest rates, from growth to demography, economists have attempted to gauge the impact of reserve accumulation. Francis and Veronica Warnock of the University of Virginia concluded that foreign-bond purchases lowered yields on ten-year Treasuries by around 0.8 percentage points in 2005. A recent working paper by researchers at the European Central Bank found a similar effect: increased foreign holdings of euro-area bonds reduced long-term interest rates by about 1.5 percentage points during the mid-2000s.

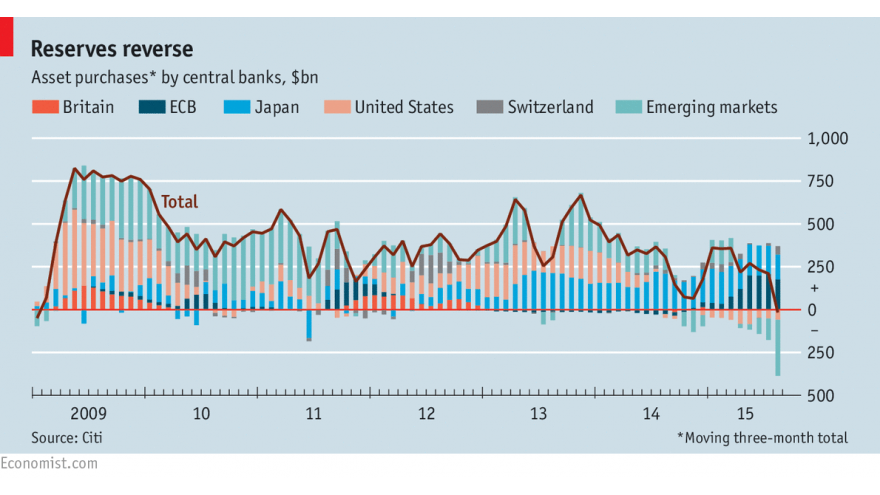

A DEFINING feature of the world economy over the past 15 years was the unprecedented accumulation of foreign-exchange reserves. Central banks, led by those in China and the oil-producing states, built up enormous hoards of other countries’ currencies. Global reserves swelled from $1.8 trillion in 2000 to $12 trillion by mid-2014. That proved to be a high point. Since then reserves have dropped by at least $500 billion. China, whose reserves peaked at around $4 trillion, has burnt through a chunk of its holdings to prop up the yuan, as capital that had once gushed in started to leak out. Other emerging markets, notably Russia and Saudi Arabia, have also called on their rainy-day stashes.

This has sparked warnings that the world faces a liquidity squeeze from dwindling reserves. When central banks in China and elsewhere were buying Treasuries and other prized bonds to add to their reserves, it put downward pressure on rich-world bond yields. Running down reserves will mean selling some of these accumulated assets. That threatens to push up global interest rates at a time when growth is fragile and financial markets are skittish. Analysts at Deutsche Bank have described the effect as “quantitative tightening”. In principle, rich-world central banks can offset the impact of this by, for instance, additional “quantitative easing” (QE), the purchase of their own bonds with central-bank money. In practice there are obstacles to doing so.

That one country’s reserves might influence another’s bond yields was expressed memorably in 2005 by Ben Bernanke, then a governor at the Federal Reserve and later its chairman, in his “global saving glut” hypothesis. Large current-account surpluses among emerging markets were a reflection of excess national saving. The surplus capital had to go somewhere. Much of it was channelled by central banks into rich-world bonds held in their burgeoning reserves. The growing stockpiles of bonds compressed interest rates in the rich world.

Yet there are doubts about how tightly reserves and bond yields are coupled. Claudio Borio of the Bank for International Settlements and Piti Disyatat of the Bank of Thailand have noted that Treasury yields tended to rise in 2005-07 even as capital flows into America remained strong, and that rates then fell when those inflows slackened. The link has been rather weak this year, too. Reserves have been run down but bond yields in both America and Europe have also fallen.

One explanation is that domestic variables outweigh foreign ones. Bond-buying by the Federal Reserve during its QE programme in 2008-14 mattered more in setting America’s long-term interest rates than increased reserve allocation by foreign central banks. In the past half year, the European Central Bank’s QE has had a dampening effect on euro-area yields. This suggests that changes in foreign-exchange reserves are not an insurmountable force. To the extent that a decline causes unwanted tightening, central banks in the rich world can counter it by buying bonds. Then again, although asset sales by central banks in emerging markets now exceed purchases by their counterparts in the rich world (see chart), the Fed shows little appetite to resume QE.

There may be other mitigating factors. The capital leaving emerging markets has not vanished. Much of it has ended up back where it originally came from. If a Chinese billionaire wants to take his cash out of the country, say, he can trade his yuan for dollars by various illicit means. That reduces China’s currency reserves, namely its holdings of American bonds. The billionaire then uses the cash to buy a home in Los Angeles. The seller of that home puts the proceeds in a local bank, which, in turn, may use the deposit to buy American bonds.

Lost and found

It is the countries that amassed reserves in the first place that probably have more to worry about. When their central banks began buying foreign assets, they paid for them with newly printed money, thereby increasing the money supply. As they switch from buying foreign assets in order to suppress their currencies to selling those assets in order to prop them up, they will correspondingly shrink the stock of money.

But even these concerns may be overdone. Reserves are not the only determinant of domestic money supply. Central banks soaked up much of the money created when they initially accumulated reserves, thus “sterilising” the impact. They can now undo that, for instance, by lowering the amount of money banks must keep at the central bank, as China has been doing. And just as central banks in the rich world use open-market operations—buying and selling domestic assets on a daily basis—to influence short-term interest rates, so can those in the developing world. Such operations require skill and deep capital markets, however.

Authorities have one more crude brake on quantitative tightening: capital controls. China has clamped down on cash outflows in recent weeks and its reserves, which fell by $95 billion in August, dropped by a less alarming $43 billion in September. If money breaks through its barriers and surges out again, China might be forced to devalue the yuan for a second time. With anxiety about the world economy rising, many hope the dam will hold for a little longer.

Comments